Hello, in this lecture, we will define Form 940 according to fundamental accounting principles. The 22nd edition defines Form 940 as an IRS form used to report employers' federal unemployment tax (FUTA) on an annual filing basis. When we think about Form 940, we are talking about a payroll tax. Typically, when we discuss payroll tax, we are referring to the FICA tax, which includes Social Security and Medicare. However, in this case, we are specifically referring to the federal unemployment tax, which is only an employer tax. It is not deducted from employee wages, but it is based on the employee wages. The Form 940 is filed annually, rather than quarterly. On the quarterly 940 form, we report Medicare, Social Security, and federal unemployment tax. However, the annual 940 form is mainly focused on federal unemployment tax, which is generally a smaller amount compared to other payroll taxes. The form itself resembles the 2016 form available on irs.gov. It includes business information at the top. To calculate the tax liability, we multiply the employee wages by the tax rate, but there is a cap on the wages, typically around $7,000. This means that most employees will reach this cap if they have been employed for a significant part of the year. We then multiply the capped wages by the tax rate to determine the liability. We compare this liability to the payments already made throughout the year. Similar to Form 1040 for individuals, the IRS expects payments to be made throughout the year, and this form simply confirms the payments made. However, unlike Form 1040, which often results in a refund due to larger withholdings than the actual tax owed, Form 940 should be more exact since it is a flat tax rate. By the end of the year, we should file...

Award-winning PDF software

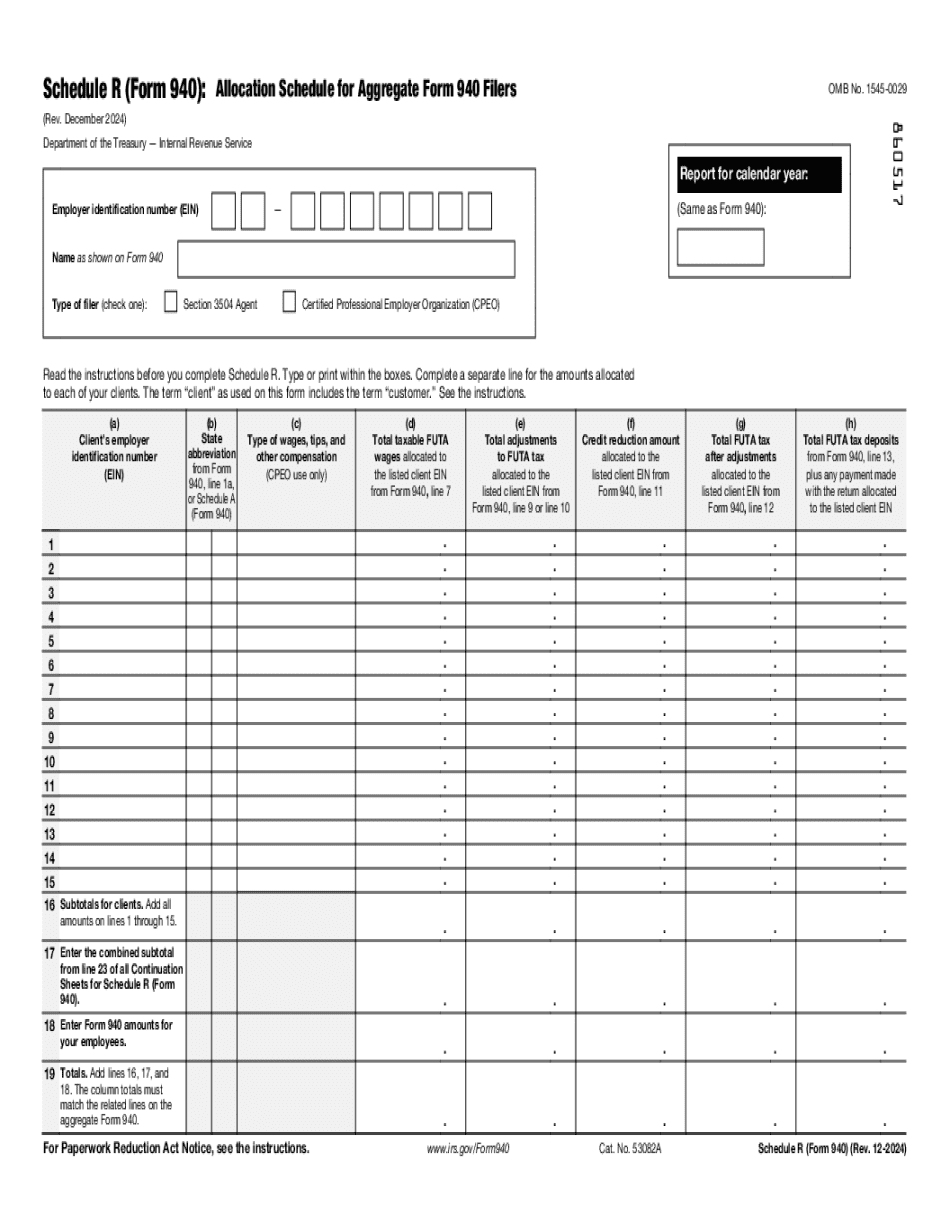

Video instructions and help with filling out and completing What 940 Schedule Return